When people hear “housing crisis” now, they mostly think of soaring rents and tight rental markets, but millions of underwater mortgages are still holding back the economy (along with stagnant wages, less job security, lower quality jobs, and other economic ills).

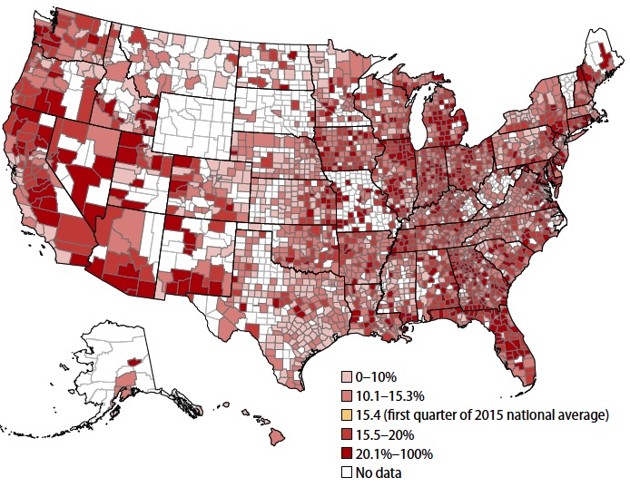

While the percentages of underwater homes have dropped in some major urban areas, these numbers are stagnant or actually going up in many rural areas, and some cities and regions. The distribution of underwater homes is very uneven across the country (see map above). Being underwater affects consumer behavior in numerous adverse ways:

While the percentages of underwater homes have dropped in some major urban areas, these numbers are stagnant or actually going up in many rural areas, and some cities and regions. The distribution of underwater homes is very uneven across the country (see map above). Being underwater affects consumer behavior in numerous adverse ways:

“When homes are underwater, their owners can’t draw on their home equity to invest in education or other big-ticket items. They also can’t rely on that equity as an option in the event of an emergency. It also makes selling their home an unappealing choice. Owners often cut back on spending and remain stuck in a state of limbo. As they wait to see whether the banks foreclose, they often don’t know if they’ll be able to stay in their homes, or even rent an apartment in the same school district. A large number of homeowners with negative equity isn’t just bad for individual families, it can have profound implications for the economy, especially when it’s in as uncertain a state as it is now. A flood of foreclosures on the market can drive down the values of other homes nearby, decreasing equity across a community.”

(Read story here.) Another problem, not mentioned in that paragraph, is that people trapped in homes they can’t sell are unable to relocate to areas of job growth; this deprives employers of workers and deprives workers of employment opportunities. Hopefully, anyone looking to move will find the area and house of their dreams soon enough. When it comes to the moving process, it can be quite stressful, especially with how much needs to be transported to and from the old house to the new one. With this being said, with the assistance of friends/family and a vehicle moving company like Cars Relo, this shouldn’t be as tough as people may think.

While our culture still clings to some vestiges of moralizing about debt (Shakespeare wrote, “neither a lender nor borrower be,” and Jesus chased the usurers out of the Temple), the entire American economy is based on risk-taking, credit, and occasional failure. You’re supposed to relocate for that promotion or better job opportunity; the economy is most efficient and prosperous when talent is free to rise to the top. You’re supposed to take out bank loans to start a business or buy a new car or college education; in the aggregate, such borrowing raises incomes and makes the whole country more prosperous.

It’s true that some small businesses fail, and some people lose jobs (or quit jobs that didn’t work out), sometimes because they reached too far, other times for reasons beyond their control; but in all cases, the bankruptcy system offers them a way out and a fresh start — because the economy benefits most when these failures don’t permanently sink entrepreneurial and individual effort. Many successful people have come back from initial failures to build successful Photo: Home Sour Home businesses, create jobs, and prosper.

It’s true that some small businesses fail, and some people lose jobs (or quit jobs that didn’t work out), sometimes because they reached too far, other times for reasons beyond their control; but in all cases, the bankruptcy system offers them a way out and a fresh start — because the economy benefits most when these failures don’t permanently sink entrepreneurial and individual effort. Many successful people have come back from initial failures to build successful Photo: Home Sour Home businesses, create jobs, and prosper.

Consequently, a certain amount of expected failure is baked into the system: Banks expect to write off a certain percentage of loans, and set loan rates accordingly; some student loans won’t be repaid; some homeowners won’t be able to keep up their mortgage payments because of job loss, illness, or other factors. In a smoothly functioning economy, these financial losses are actuarially predictable with a high degree of accuracy — and the system works. Of course, in a true crisis, this system breaks down — and that’s when massive government intervention is appropriate and necessary.

Trouble is, the intervention this time didn’t help most of those who needed it most. It bailed out Wall Street and the banks, and speculators did just fine. But nobody else did. The housing crisis could have been resolved a long time ago if banks had moved swiftly to clear the market of foreclosed properties, and had cooperated with distressed borrowers on loan workouts, principal reductions, and other strategies to get the unpayable debts out of the system so the economy could move forward. Unfortunately, the big banks — who bear heavy responsibility for creating the crisis in the first place — didn’t fulfill their role.

As a result, the nation ended up saddled with debts that acted as an anchor chain dragging down the American economy. And there was no accountability, either for the criminal acts of unethical bankers, or for the financial damage they caused, other than the Obama administration’s questionable policy of extracting approximately $100 billion of fines from the big banks, which inured solely to the benefit of the federal government, in exchange for no criminal prosecutions. Meanwhile, distressed borrowers were left languishing, effectively thrown under the bus.

The result is a stagnant economy, young people who can’t afford to start families, millions of homeowners who can’t move, and millions of former homeowners competing for a limited supply of rental housing and driving rents to levels unaffordable for nearly everyone — and a demoralized and dispirited nation whose people wonder if they have a future. The rental housing supply can also begin to decrease when landlords start to consider selling rental property for circumstances such as needing the extra money or not wanting to continue with having this level of responsibility. And if they decide to move back into that property, then the limited rental supply becomes even narrower. Therefore, even though it’s hard, people are still looking to buy property in and around places that seem quite feasible according to the market standards.

Obama’s policies, on the whole, undoubtedly were better than the alternatives offered by McCain and Romney. The Federal Reserve, with no help from Congress after the Republican midterm sweeps of 2010 and 2014, probably saved America from another 1930s-scale Great Depression. Saving the banking system, stanching the job losses, and returning the economy to growth — however tepid — obviously were the top priorities. And Obama and his appointees got the priorities right.

But one of the great tasks left undone by his administration was shaking bad debt out of America’s financial system, and that’s a task the next administration must tackle if our economy is ever to return to healthy growth. Sen. Elizabeth Warren has come up with concrete proposals for removing the albatross of student debt from the young generations, which have no hope of being enacted as long as Republicans control Congress.

The financial industry and banks will resist anything approaching bankruptcy reform and real mortgage relief, but those issues too must be forced to a resolution, if the economy is the growth and provide good jobs again. There’s nothing good about bad debt, and the best thing for everyone is to get rid of it through debt restructurings, writeoffs, and bankruptcy — giant corporations do that all the time, without protest from the banks or Wall Street, so why is this relief denied to small businesses, homeowners, and students unable to get decent jobs in an economy that demands ever-greater educational credentials but at the same time won’t pay living wages?

The bottom line is that debt-distressed households and individuals aren’t consumers. They can’t borrow, and they can’t buy stuff. They can’t get married, have children, and send them to college; or buy houses, cars, furnishings, and vacations. And as long as our fellow citizens remain hamstrung by paper debts that aren’t ever going to be paid anyway, various kinds of dislocations and drags will continue to exist in our markets and economy.